A latent risk associated with probable increases in interest rates is the currency composition of debt issued by non-financial corporations in emerging markets.

The Fed is expected to begin raising interest rates in September this year, the first rate hike since 2006. A likely consequence will be an inflow of capital, since the monetary policies of other central banks remain loose.

Expecting higher returns on US bonds, investors will be attracted to dollar-denominated assets, paving the way for the continued appreciation of US dollar.

This is a game changer.

Low interest rates, compressed term premia, appreciation in many EME currencies, and better access to international markets mean that corporations have had ample incentive to ramp up leverage post-2008, and a non-negligible share of the borrowing has been denominated in foreign currency — especially in US dollars.

Monetary tightening in the US has several corollaries — inflation is subdued, US companies’ sales in foreign currency areas are diminished, and dollar-denominated debt outside the US becomes much costlier to service.

The low rate environment has whetted the appetite for dollar debt of corporations in emerging markets, which face much higher lending rates at home. Since the financial crisis, dollar debt owed by non-financial corporations outside US has increased by 50 percent, and currently stands at $9 trillion.

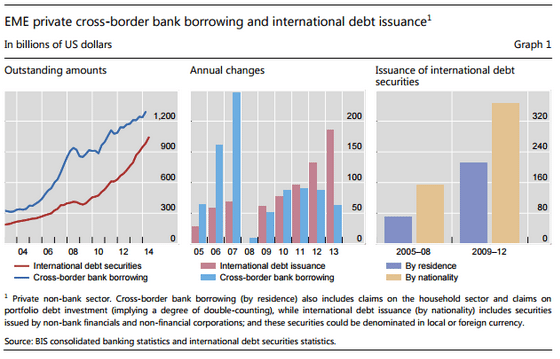

Research from the Bank of International Settlements (BIS) points to rising trends in issuance of debt in international markets, as shown in Graph 1. In China alone, loans in US dollars have jumped from $200bn in 2008 to over $1 trillion today.

As events in Ukraine show, debt can quickly become unsustainable, especially when geopolitical risks affect the exchange rate and increases the local currency value of foreign currency liabilities.

Roughly half of Ukraine’s public debt is denominated in foreign currency, so as the hryvnia depreciates, the debt burden rises. It highlights the issue of whether not just public, but also private sector liabilities, are properly hedged (e.g. using derivatives) and/or matched by foreign currency assets or returns.

When risks materialize – be they geopolitical, monetary or exchange rate-driven – the credit worthiness of highly leveraged corporates can deteriorate rapidly, causing spikes in bond yields and higher financing costs. This may ultimately hurt economic growth in the domestic economy, and jeopardize local banks as well as investors holding corporate debt.

At a time when emerging market economies are already experiencing headwinds in the form of slowing growth, this cocktail of dollar appreciation and rising bond yields could diminish it even further. As exemplified in the above charts, the number of stakeholders have increased markedly over the past years, so the losses could be substantial.

Foreign currency debt burdens means that exchange rate shocks can activate detrimental feedback loops, such as by a double whammy of amplified default risk and pressure to deleverage in case of domestic depreciation.

Concerns rising from such a combination of events could then cause “widespread rout of international investors, loss of market access and spillovers into domestic interbank markets – exacerbating the financial and macroeconomic impact of the initial interest rate or foreign exchange shock.”

Investors should keep a close eye on the asset composition of corporates. If increased borrowing reflects stronger earnings prospects, as often seen in case of higher investment and capital expenditure, this may offset the risk associated with debt denominated in foreign currency.

Conversely, there is greater risk associated with corporate debt issued by firms engaging in speculative activity by exploiting access to international, cheap financing, just to deposit the borrowed funds at home and earn the interest rate differential.

Furthermore, sectors that receive a lot of their revenue in foreign currency, such as commodity producers, are less exposed than domestically-oriented sectors, like telecoms, construction and utilities.

Combining these aspects suggests that liquid, deep markets for derivatives and other hedging instruments are an advantage in the face of currency mismatches in corporate debt. Given the lack of a well-developed hedging market, “mismatches will often go unhedged because markets may not be deep enough to provide appropriate and cost-effective hedging.” A prime example of un-hedged, domestically-oriented corporates is Chinese property developers.

sourche: http://globalriskinsights.com/2015/06/private-sector-debt-in-emes-poses-risk-as-us-dollar-appreciates/

Δεν υπάρχουν σχόλια:

Δημοσίευση σχολίου